All Categories

Featured

Table of Contents

TIAA may offer a Commitment Reward that is just readily available when electing lifetime earnings. Annuity contracts might contain terms for maintaining them in force. TIAA Conventional is a set annuity product issued with these agreements by Educators Insurance coverage and Annuity Organization of America (TIAA), 730 Third Method, New York, NY, 10017: Kind collection consisting of yet not restricted to: 1000.24; G-1000.4; IGRS-01-84-ACC; IGRSP-01-84-ACC; 6008.8 (guaranteed income life insurance).

Converting some or all of your financial savings to earnings advantages (referred to as "annuitization") is an irreversible choice. Once income benefit settlements have actually started, you are incapable to change to an additional option. A variable annuity is an insurance coverage contract and consists of underlying financial investments whose value is linked to market performance.

Nationwide Secure Growth Fixed Annuity

When you retire, you can pick to receive revenue forever and/or other earnings choices. The real estate sector is subject to different threats including changes in underlying residential property worths, expenses and earnings, and possible ecological obligations. Generally, the value of the TIAA Property Account will vary based on the hidden value of the straight property, genuine estate-related financial investments, genuine estate-related safety and securities and fluid, fixed revenue financial investments in which it invests.

For a more complete discussion of these and other dangers, please speak with the program. Liable investing incorporates Environmental Social Governance (ESG) aspects that might affect direct exposure to companies, markets, markets, restricting the type and number of financial investment chances available, which might result in excluding investments that do well. There is no guarantee that a varied portfolio will certainly boost overall returns or surpass a non-diversified portfolio.

Is A Lifetime Annuity A Good Investment

Over this exact same period, correlation between the FTSE Nareit All Equity REIT Index and the S&P 500 Index was 0.77. Index returns do not reflect a reduction for costs and costs.

10 TIAA may state added amounts of interest and revenue benefits above contractually ensured degrees. Once income advantage repayments have actually begun, you are not able to transform to an additional alternative.

It's crucial to keep in mind that your annuity's equilibrium will certainly be lowered by the income repayments you receive, independent of the annuity's efficiency. Income Test Drive income payments are based upon the annuitization of the amount in the account, duration (minimum of one decade), and various other factors selected by the participant.

Annuitization is irrevocable. Any kind of guarantees under annuities released by TIAA are subject to TIAA's claims-paying capacity. Interest in unwanted of the ensured amount is not ensured for periods other than the periods for which it is stated.

Scan today's checklists of the most effective Multi-year Guaranteed Annuities - MYGAs (updated Sunday, 2024-12-01). These listings are sorted by the surrender charge period. We change these lists daily and there are regular adjustments. Please bookmark this web page and return to it commonly. For specialist assist with multi-year assured annuities call 800-872-6684 or click a 'Get My Quote' button alongside any kind of annuity in these lists.

Deferred annuities permit a quantity to be withdrawn penalty-free. Deferred annuities typically permit either penalty-free withdrawals of your gained interest, or penalty-free withdrawals of 10% of your agreement worth each year.

Which Of These Is True Of An Annuity

The earlier in the annuity period, the greater the penalty percent, referred to as abandonment fees. That's one reason it's ideal to stick with the annuity, as soon as you devote to it. You can take out whatever to reinvest it, yet prior to you do, see to it that you'll still triumph by doing this, even after you figure in the abandonment fee.

The abandonment fee could be as high as 10% if you surrender your contract in the very first year. A surrender fee would certainly be billed to any withdrawal higher than the penalty-free quantity permitted by your delayed annuity contract.

When you do, it's finest to persevere throughout. Initially, you can establish "organized withdrawals" from your annuity. This suggests that the insurer will send you payments of interest monthly, quarterly or annually. Utilizing this method will not take advantage of your initial principal. Your other option is to "annuitize" your postponed annuity.

This opens a range of payment choices, such as earnings over a solitary lifetime, joint life time, or for a specific period of years. Several postponed annuities permit you to annuitize your agreement after the very first contract year. A major distinction is in the tax obligation treatment of these items. Passion earned on CDs is taxed at the end of annually (unless the CD is held within tax certified account like an IRA).

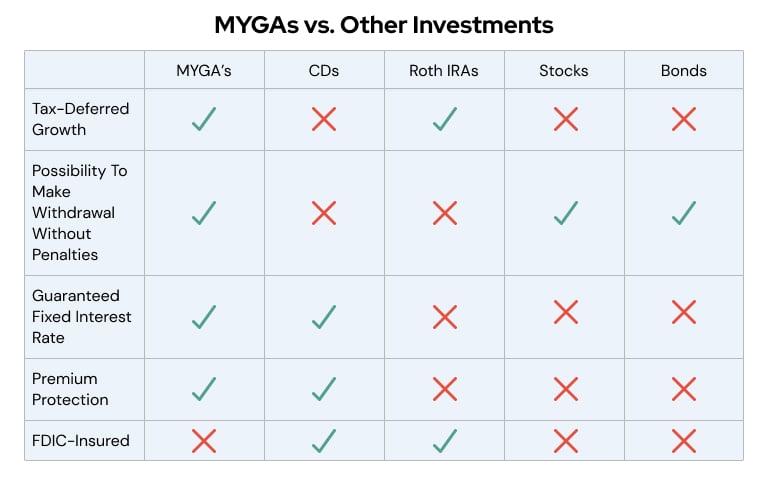

The passion is not tired till it is gotten rid of from the annuity. To put it simply, your annuity expands tax deferred and the interest is worsened annually. Nonetheless, comparison buying is constantly a good concept. It's true that CDs are guaranteed by the FDIC. MYGAs are insured by the individual states normally, in the array of $100,000 to $500,000.

Yet prior to pulling money out of a MYGA early, take into consideration that a person of the significant advantages of a MYGA is that they expand tax-deferred. Chris Magnussen, certified insurance representative at Annuity (how long does an annuity payout).org, discusses what a repaired annuity is. A MYGA provides tax obligation deferment of rate of interest that is worsened on a yearly basis

Can You Take Money Out Of Your Annuity

It resembles investing in an individual retirement account or 401(k) however without the payment restrictions. The tax obligation rules modification a little depending on the kind of funds you utilize to buy the annuity. If you acquire a MYGA with certified funds, such via an individual retirement account or various other tax-advantaged account, you pay revenue tax obligation on the principal and rate of interest when you obtain money, according to CNN Money.

This tax advantage is not distinct to MYGAs. It exists with typical set annuities. MYGAs are a sort of taken care of annuity. The primary difference between conventional fixed annuities and MYGAs is the time period that the contracts ensure the fixed rates of interest. MYGAs assure the interest price for the whole duration of the contract, which might be, for instance, ten years.

So, you may acquire an annuity with a seven-year term yet the price might be guaranteed only for the first three years. When individuals speak of MYGAs, they usually compare them to CDs. Discover exactly how to safeguard your nest egg from market volatility. Both MYGAs and CDs deal ensured rate of return and a guaranty on the principal.

Contrasted to investments like stocks, CDs and MYGAs are much safer however the price of return is reduced. who guarantees annuities. They do have their differences. A CD is issued by a bank or a broker; a MYGA is a contract with an insurer. A CD is FDIC-insured; a MYGA is not guaranteed by the federal government, however insurer should belong to their state's warranty organization.

Ira Annuities

A CD might have a lower passion price than a MYGA; a MYGA may have extra charges than a CD. CD's might be made offered to creditors and liens, while annuities are protected versus them.

Offered the conventional nature of MYGAs, they may be better suited for customers closer to retirement or those that choose not to be based on market volatility. "I transform 62 this year and I really want some kind of a fixed price as opposed to bothering with what the securities market's going to perform in the following 10 years," Annuity.org client Tracy Neill stated.

For those that are wanting to exceed inflation, a MYGA might not be the best monetary strategy to satisfy that purpose. If you are seeking an option to replace your earnings upon retired life, other sorts of annuities might make more feeling for your economic objectives. Furthermore, other kinds of annuities have the possibility for higher benefit, but the threat is higher, also.

Better comprehend the steps associated with acquiring an annuity. Multi-year ensured annuities are a type of taken care of annuity that deal guaranteed rates of return without the risk of securities market volatility. They use modest returns, they are a risk-free and reliable financial investment choice. A market worth adjustment is a feature an annuity company might include to protect itself against losses in the bond market.

Before pulling cash out of a MYGA early, think about that one of the significant advantages of a MYGA is that they grow tax-deferred. Chris Magnussen, certified insurance coverage agent at Annuity.org, explains what a repaired annuity is. A MYGA uses tax obligation deferral of interest that is worsened on an annual basis.

It's like investing in an IRA or 401(k) yet without the payment limits.

Aaa Fixed Annuity

It exists with typical fixed annuities. The primary difference in between traditional set annuities and MYGAs is the period of time that the agreements assure the fixed rate of interest rate.

You may purchase an annuity with a seven-year term however the rate might be assured only for the first three years. Discover how to safeguard your nest egg from market volatility.

Compared to financial investments like stocks, CDs and MYGAs are much safer yet the price of return is lower - new york life and annuity. A CD is released by a financial institution or a broker; a MYGA is a contract with an insurance policy company.

A CD may have a reduced rate of interest rate than a MYGA; a MYGA might have a lot more costs than a CD. CD's might be made readily available to financial institutions and liens, while annuities are secured versus them.

Offered the conservative nature of MYGAs, they could be better for customers closer to retired life or those who favor not to be subjected to market volatility. "I turn 62 this year and I really want some type of a fixed price rather than bothering with what the securities market's mosting likely to carry out in the next 10 years," Annuity.org consumer Tracy Neill claimed.

Fixed Deferred Annuity Definition

For those that are seeking to outpace rising cost of living, a MYGA may not be the most effective monetary method to satisfy that goal. If you are looking for a service to change your income upon retired life, other sorts of annuities might make more sense for your monetary goals. Furthermore, other kinds of annuities have the capacity for greater incentive, however the danger is greater, also.

Much better recognize the steps associated with acquiring an annuity. Multi-year ensured annuities are a kind of dealt with annuity that deal assured rates of return without the risk of stock market volatility. They use moderate returns, they are a secure and trustworthy financial investment option (annuity will). A market worth adjustment is a feature an annuity provider may consist of to shield itself versus losses in the bond market.

{kind=link}

Table of Contents

Latest Posts

Breaking Down Annuity Fixed Vs Variable Key Insights on Fixed Vs Variable Annuities Breaking Down the Basics of Fixed Annuity Or Variable Annuity Benefits of Choosing Between Fixed Annuity And Variabl

Decoding Retirement Income Fixed Vs Variable Annuity Everything You Need to Know About Annuity Fixed Vs Variable Defining the Right Financial Strategy Advantages and Disadvantages of Immediate Fixed A

Exploring the Basics of Retirement Options A Closer Look at How Retirement Planning Works What Is the Best Retirement Option? Features of Immediate Fixed Annuity Vs Variable Annuity Why Choosing the R

More

Latest Posts